Navigating the U.S. Industrial Real Estate Landscape in 2025: Challenges, Opportunities, and Strategies

Executive Summary

The United States industrial real estate market is undergoing a major evolution. Following unprecedented demand fluctuations driven by the pandemic, it’s now poised to stabilize as we approach 2025. The market is showing a shift back to pre-pandemic demand drivers, propelled by e-commerce growth, increased outsourcing to third-party logistics providers (3PLs), and supply chain adaptations like onshoring. However, significant challenges remain—particularly for aging warehouse spaces struggling to compete against modern facilities. This white paper explores these dynamics, offering data-driven insights into leasing trends, development opportunities, and strategic recommendations for stakeholders navigating this transformation.

Current Market Conditions for Old and New Warehouse Spaces

The Rise of Modern Facilities

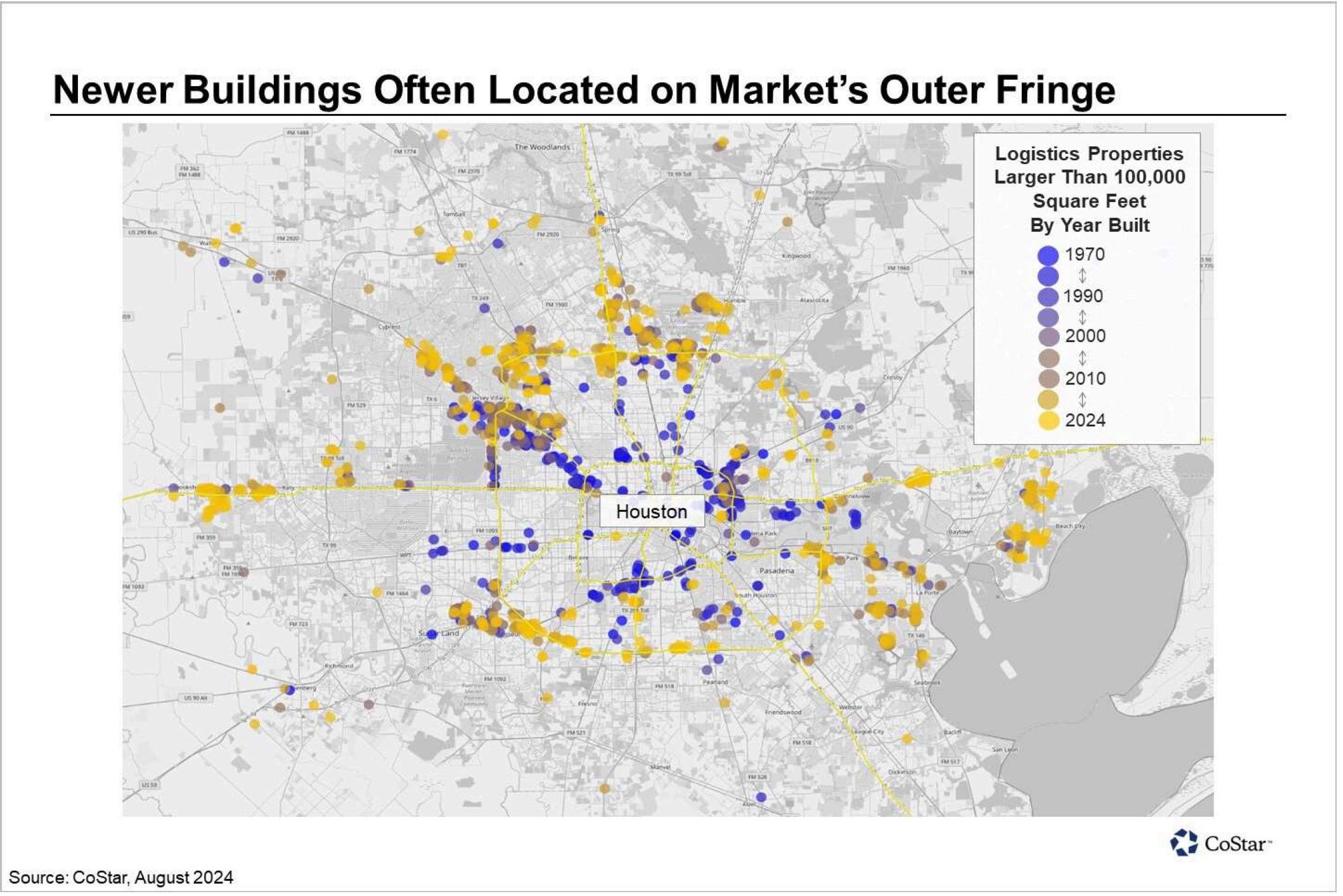

Demand for new warehouse spaces is robust. Modern, first-generation facilities that prioritize efficiency and advanced technology have captured the market’s attention, resulting in positive net leasing absorption. Nearly 400 million square feet of industrial space constructed since 2023 remained vacant by the third quarter of 2024, but this is primarily attributed to their substantial capacity to meet increasing demand. Furthermore, buildings constructed post-2000 far outperform their older counterparts, accounting for over 200 million square feet of positive absorption, while facilities built before 2000 saw 100 million square feet of negative absorption last year.

Latest reports indicate 135 million square feet (msf) net absorption in 2024, a modest yet steady recovery, signaling resilience amidst industry headwinds. However, challenges persist, with vacancy rates climbing to 6.7%, the highest since pre-pandemic years, and greater reliance on high-quality, newly-built logistics hubs. This white paper examines these dynamics, highlights ongoing challenges, and offers actionable recommendations for developers, investors, and professionals navigating the landscape.

State of the Market

Demand for Quality Fuels Shift Away From Older Spaces

Older distribution centers face mounting challenges in leasing activity. Properties constructed prior to 2000 accounted for over 100 msf of negative absorption in 2024, as tenants prioritize facilities offering high ceilings, energy efficiency, and automation capabilities. This contrasts with 200 msf of positive absorption posted by post-2022 constructions, highlighting the flight to quality within the tenant landscape.

Occupiers expect warehouses to align with modern operational priorities, from automated inventory systems to layouts optimized for last-mile delivery—a critical factor given e-commerce’s anticipated growth from 23.2% of total retail sales to 25% by late 2025. Older spaces, often situated in secondary markets or configured for outdated needs, are becoming less attractive without significant upgrades, pushing many owners toward capital-intensive retrofits or sales strategies.

Key Market Drivers

Economic Trends

Economic normalization post-pandemic is refocusing industrial real estate fundamentals on classical demand drivers, such as consumer spending and retail expansion. However, uncertainty tied to rising interest rates and a decelerating GDP presents a mixed outlook. Despite these headwinds, industrial leasing remains strong, with an expected stabilization in activity at 800 million square feet of deals in 2025.

Offshoring is rapidly being counterbalanced by onshoring and nearshoring to North America, especially Mexico, as part of supply chain resiliency strategies. With record-low industrial vacancy rates in Mexico, U.S. distribution sites located close to border regions or along key highways like Interstates 29 and 35 are increasingly critical in facilitating product storage and distribution.

Supply Chain Demands and the Role of E-Commerce

The e-commerce revolution remains a defining trend, accounting for 23.2% of U.S. total retail sales in Q3 2024, projected to reach 25% by the end of 2025. This growth amplifies the demand for sophisticated warehouses equipped with fulfillment technology, particularly in urban-adjacent areas that enable rapid last-mile delivery. The dominance of Amazon-inspired operational models drives stakeholders to rethink the strategic location, scale, and automated infrastructure of facilities.

Furthermore, 3PLs now play an outsized role in industrial leasing. Companies increasingly outsource logistics operations to enhance flexibility for inventory management, reduce capital lockups, and better focus on core areas like product development. With 3PLs expected to represent 35% of industrial leasing activity next year, their growth underscores a broader shift toward outsourced operational efficiency.

Technological Advancements

Technology enables occupiers to optimize warehouse efficiency and future-proof their facilities. Features like autonomous robotics, smart inventory systems, and energy-efficient building systems are no longer optional—they’re becoming necessities for tenants aiming to stay competitive. Facilities unable to meet these technological thresholds are at risk of obsolescence, further deepening the divide between new and old industrial spaces.

Regional Dynamics and Investment Highlights

Vacancy Rates

Vacancy rates increased by 20 basis points (bps) in Q4 2024 alone, reaching 6.7%, though the pace of vacancy growth is slowing compared to previous years. Big-box facilities (over 300,000 sq ft.), which accounted for 51% of new speculative deliveries, face a 10.7% vacancy rate—higher than the national average.

Markets heavily impacted by speculative projects, such as Austin (13.3%), Phoenix (12.7%), and Greenville, SC (11.6%), report overwhelmingly high vacancy rates relative to more stable core hubs like the Inland Empire (8.0%) or Dallas/Ft. Worth (9.7%).

Construction Trends

Despite challenges like fluctuating interest rates and material costs, developers added 425 msf of new industrial supply in 2024, with 85.3 msf in Q4 alone. This marks the lowest delivery volume since mid-2021, indicating reduced speculative activity moving toward 2025. Over 78% of 2024 completions consisted of speculative builds, explaining heightened vacancy pressure on non-premium facilities in overbuilt markets. Across active developments, smaller projects of 100,000-300,000 sq ft. dominate pipelines, representing 60%+ of construction underway.

Net Absorption & Leasing Activity

Net absorption totaled 36.8 msf in Q4 2024, reflecting a 10.5% quarter-over-quarter increase but emphasizing disposition stagnation within speculative projects. Though leasing slowed compared to 2020-2022 highs, overall demand stabilized with 800 msf projected for 2025, with third-party logistics (3PL) firms continuing to hold a 35% market share of new leasing activities.

Strategic Recommendations for Stakeholders

Regional Variances & Emerging Hubs

Core Markets Steady Leasing

Regions like Atlanta, Dallas/Ft. Worth, Inland Empire, and New Jersey remain indispensable for industrial occupiers due to their access to consumer pools, established trade nodes, and robust supply chain networks. For instance, Dallas/Ft. Worth achieved 3.3+ msf Q4 absorption, ensuring its position as a leasing stalwart.Rising Opportunities in Emerging Nodes

Secondary hubs are rapidly positioning themselves as alternatives to oversaturated areas. Highlights include Louisville (+38% pipeline growth YOY) for manufacturers and Phoenix (42.9 msf delivered) catering to spillover demand from constrained West Coast ports. Proximity to resurgent U.S.-Mexico corridors is accelerating demand in San Antonio, Austin, and Kansas City.Onshoring Commands Cross-Border Trade

With tariffs looming on Asian imports and reshoring driving capacity increases for electronics and automobiles, emerging southwestern hubs along Interstates 29/35 are capturing industrial traffic at record growth levels.

For Developers

Focus on High-Quality Construction

Capitalize on the flight to quality by emphasizing developments with advanced logistics systems, sustainability certifications, and scalability to meet tenant needs.Adapt Older Spaces for Niche Markets

Reposition outdated properties by targeting smaller manufacturers or own-occupy buyers who value cost savings over ultra-modern features.Leverage Emerging Market Potential

Explore secondary cities where industrial land remains affordable, and long-term growth is supported by increasing e-commerce penetration and trade activity.

For Investors

Prioritize Core Market Assets

Assets in major industrial hubs will remain resilient, providing predictable returns bolstered by robust tenant demand.Identify Value-Add Redevelopment Opportunities

Acquire and modernize older facilities, tailoring them to underserved niches like cold storage or local distribution networks.Bet Long-Term on Nearshoring

Markets linked to U.S.-Mexico trade will see consistent value appreciation. Analyze infrastructure projects to secure footholds in these hotspots.

For Occupiers

Secure Space Early

The balanced demand-supply equation is shifting, and locking in favorable lease terms now will hedge against steep cost increases in coming years.Invest in Automation-Friendly Locations

Tenants should seek spaces with high ceilings, flat floors, and the electrical capacity needed for robotics, ensuring operational scalability.Utilize 3PL Services

Partnering with 3PLs can reduce upfront capital risks while providing the flexibility to adapt logistics in uncertain climates.

Concluding Thoughts

The industrial real estate market in the United States stands at a pivotal juncture. The insights presented in this white paper reflect a sector navigating dynamic shifts driven by evolving technology, supply chain demands, and the enduring impact of e-commerce. Key findings underscore the challenges faced by aging distribution centers amid tenant preferences for modern, high-performing facilities. Simultaneously, speculative oversupply in certain markets has created mixed occupancy landscapes, where core and emerging hubs race to define their future roles within the industry’s framework.

Yet amidst these challenges lie clear opportunities. Developers and investors who align with current demand signals—whether through retrofitting legacy spaces, building sustainable facilities, or investing in forward-looking locations—are poised to lead the next wave of growth. Solutions leveraging energy-efficient construction, last-mile delivery optimization, and scalable logistics offer stakeholders the chance to address the industry’s bottlenecks while setting new standards for resilience and efficiency.

Beyond immediate gains, the broader implications of these advancements ripple across the industrial real estate landscape. E-commerce growth, reshoring efforts, and the drive for net-zero operations will reshape practices, policies, and priorities in the coming years. Those who proactively adapt to these shifts—not only reacting to current trends but anticipating future disruptions—will unlock significant advantages in the marketplace.

The time to act is now. Decision-makers must prioritize innovative solutions and align their strategies to meet both tenant demands and sustainability goals. Developers, investors, and occupiers alike are encouraged to engage with these challenges and transform them into opportunities to lead a rapidly evolving industry. By committing to smarter, more adaptive practices today, stakeholders can ensure that their contributions shape a longer-term vision for a resilient and thriving industrial real estate future.

Take the first step—align your strategies, adopt innovative solutions, and be part of the transformation driving the industry forward. The success of tomorrow begins with the decisions you make today.